The Credit Roadblock for MSMEs

Despite contributing nearly a third of India’s GDP and employing over 110 million people, MSMEs still face a pronounced credit gap—driven by lack of collateral, inadequate records, regional disparities, delayed payments, and slow adoption of digital solutions. The gap is widest among micro- and women-led businesses, and in services and trading sectors. Read More >>

The Union Budget 2025-26 outlines several initiatives designed to bolster the Micro, Small, and Medium Enterprises (MSME) sector, acknowledging its vital contribution to India’s economic progress alongside agriculture, investments, and exports. To support business growth and enhance efficiency, the budget has increased the investment and turnover thresholds for MSME classification. Additionally, access to credit is expected to improve through a higher credit guarantee cover for micro and small enterprises, startups, and MSMEs engaged in exports. However, Small and Medium Enterprises (SMEs) in India face significant challenges when it comes to accessing and managing credit. These challenges persist despite the sector’s critical role in economic growth, job creation, and exports.

Formal Credit Access:

Credit Gap: India’s MSME sector faces a significant credit gap, estimated at ₹30 lakh crore (about 24% of total credit demand). Only about 19% of MSME credit demand is met through formal channels, according to recent government and SIDBI-backed reports.

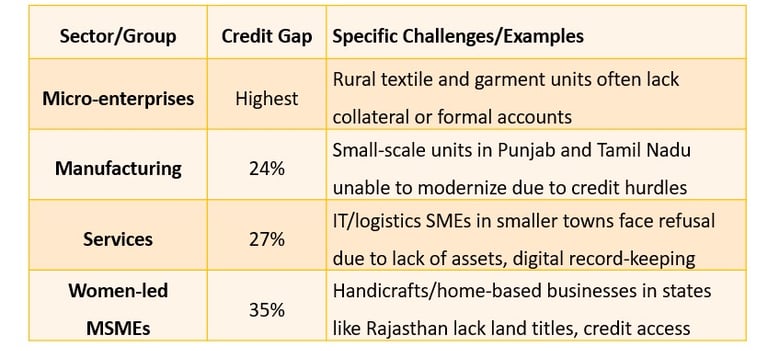

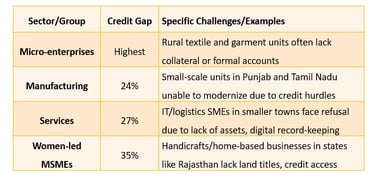

Growth and Disparities: Although credit supply has grown, the gap is sharper for certain groups. Medium-sized businesses have a 29% gap, while micro and small businesses also find it hard to access sufficient funds. MSMEs involved in trading face the widest gap at around 33%, primarily due to a lack of collateral

Collateral and Documentation:

Manufacturing: Among SMEs, especially in textiles and apparel hubs like Tiruppur and Ludhiana, many businesses lack land or property documents and often maintain informal accounts. This prevents them from meeting collateral requirements set by banks

Service Sector: The services sector suffers more, with a credit gap of 27%. Businesses in logistics and small IT services, often based outside major metropolitan areas, generally have few fixed assets and largely depend on cash-based sales, which further limits access to formal loan

High Cost of Borrowing

Interest Rates and Additional Costs: While credit from banks to MSMEs has grown by over 24% in recent years, those who do get loans often report higher interest rates, sometimes exceeding those offered to large firms. Additional charges (processing, documentation, insurance) also raise the total cost of loans, heavily impacting profitability for smaller units

Lack of Credit History and Financial Records

Record-keeping Challenges: Many small businesses, particularly in rural and semi-urban areas, have incomplete or non-audited financial records. The formalisation drive and Udyam Registration have helped, but a large number of MSMEs remain informal, making it difficult for lenders to assess their creditworthiness

Credit History: The absence of previous formal borrowings and insufficient use of digital payment systems further restricts MSMEs from building a solid credit profile required by banks

Awareness and Information Gap

Government Schemes: Programs like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) and MUDRA loans exist, but many small businesses are unaware or unable to meet the eligibility criteria due to lack of outreach and weak financial literacy

Financial Literacy: This gap is especially acute among first-generation entrepreneurs and women-led enterprises, reducing their chances of receiving beneficial loans

Delayed Payments and Cash Flow Problems

Delayed Receivables: Pending payments to MSMEs have reached ₹21,108 crore as of late 2024, as per government data. Over 90,000 applications regarding delayed payments have been filed, with state governments and central public sector undertakings among the largest defaulters

Cash Flow Impact: Delays in payment cycles (such as 60–90 days from larger corporates or government buyers) lead to working capital shortages, which further damage SMEs’ eligibility for loans and disrupt day-to-day operations

Inequality Across Sectors and Regions

Digital Divide

Adoption Matters: Only a small portion (less than 15%) of MSMEs have adopted formal digital systems. Those who have shifted to digital payment, e-invoicing, or online sales report improved chances of getting credit

Policy Initiatives: The government now promotes digital credit scoring models to bridge documentation gaps and enable faster, data-driven loan approvals—especially for newly formalized or tech-savvy micro and small enterprises

Policy Measures and Government Steps

The CGTMSE and PM Mudra Yojana are flagship schemes aiming to make collateral-free loans up to ₹200 lakh available to eligible MSMEs.

Initiatives such as the Samadhaan Portal, set up for monitoring and resolving delayed payment grievances, are making systemic improvements.

Greater formalisation through Udyam Registration and the use of digital tools are being actively encouraged by government policies

In summary:

Despite contributing nearly a third of India’s GDP and employing over 110 million people, MSMEs still face a pronounced credit gap—driven by lack of collateral, inadequate records, regional disparities, delayed payments, and slow adoption of digital solutions. The gap is widest among micro- and women-led businesses, and in services and trading sectors. Recent years have witnessed improvements in credit disbursement and the rise of supporting government programs, but much remains to be done for truly inclusive, affordable, and reliable credit access for India’s MSMEs

Citations:

[1] Enhancing Competitiveness of MSMEs in India" (NITI Aayog/PIB)

[2] MSMEs face credit gap of Rs 30 lakh crore, women-owned highest shortfall: Tribune/SIDBI

[3] UNDERSTANDING INDIAN MSME SECTOR" (SIDBI/government report)

[4] MSMEs witness spike in credit from banks by 24%: RBI Data, ETBFSI

[5] Economic Times, MSMEs: Affordable credit, timely payments

[6] MSME Annual Report 2023–24, Ministry of MSME

[7] Women MSMEs still struggle for credit (SIDBI/government data)

[8] Pending MSME Payment Reaches Rs 21,108 Cr: Data, BusinessWorld

[9] PIB: Govt to resolve the problem of delayed payments to MSMEs

[10] ANI: Indian SMEs embrace digitalisation, sustainability: FICCI

[11] PIB Press Release on MSME credit gap